I’m going to start by saying that as someone who works in tech (and who weathered the recent downturn in that sector just fine), I cannot speak for the economic insecurity that many feel, or the extent to which inflation has affected many people’s personal finances. I can believe that the economy of recent years has inflicted hardship on many, and I sympathize.

But I’m frustrated by recent polls which consistently show that voters seem to think the solution to these woes is to re-elect Donald Trump. I believe the perception that Trump handled the economy better is completely backwards and ignores the fact that economic policies have a lagging effect on the economy. Based solely on that, one could conclude that the strong economy under Trump was largely thanks to Obama, and the challenging Biden economy is Trump’s fault.

It’s of course more complicated than that, but it’s a more reasonable conclusion than the idea that had Trump been re-elected, our economy would be any better off. Let’s look at a few factors that have contributed to the economy under Biden, and also consider whether it’s as bad as people focused on the price of eggs make it out to be.

While the stock market is not the end-all-be-all indicator of economic health, it’s a good enough proxy to start with. While the S&P 500 certainly did well under Trump, it was largely a continuation of the trend that was well underway already. Sure, the Trump tax cuts had a stimulative effect, as did persistent low interest rates, but the economy didn’t really need either - it was already doing well. In fact, it’s pretty clear now that a lot of this market performance - especially the post-COVID recovery of 2020/2021 - was fueled in large part by a low-interest-rate tech bubble. So yes, the market did well under Trump, but one could argue it did too well and that it was only a matter of time before something burst the bubble.

That “something” was interest rate rises to combat rising inflation in 2022. Inflation occurs as a result of “too much money spent chasing too few goods.” This is exactly what happened during the Biden administration, but the seeds were sown by policies and events that largely preceded it. Supply chain snarls due to COVID-19 lockdowns took a long time to recover, resulting in waves of shortages around the world (which continued into 2022 when COVID finally hit China hard). This resulted in fewer products for consumers to buy, which drives up prices. Add to that the fact that countries around the world, especially the US, spent trillions on relief funds during the pandemic. The US spent over $4 trillion on various forms of relief, including cash payments (the majority of which was passed under the Trump administration). Countries around the world effectively showered their citizens with money during a time of supply shortages. This is a textbook recipe for inflation, and unsurprisingly, it has been a worldwide phenomenon.

I don’t think it’s reasonable to conclude that in one year Biden was able to mishandle the economy so badly as to trigger a sharp increase in global inflation, though you could argue that the American Rescue Plan made things worse than they would have otherwise been. But would Trump have done better? In December 2020 he was calling for more spending, not less. And would he have pressured his Fed chairman against raising interest rates to combat inflation, out of fear of a recession? He did it before, and has recently said he might do it again. It’s not inconceivable that inflation would have actually been worse under Trump.

Rising interest rates cause economic pain and it was widely believed in 2022 that they would trigger a recession. Despite this, interest rate rises are the best tool the Fed has to fight inflation and thus a necessary step to avoid longer-lasting pain. As of this writing in late 2023, while some sectors were certainly hit hard by raising rates (debt-fueled tech startups and especially crypto), it seems that overall the Fed may have managed the fabled “soft landing.” Inflation isn’t as low as they’d like, but it’s come down, and so far we’ve managed to avoid a broad-based recession. The market hasn’t been on a tear, but if you look at that chart above, neither has it crashed. We’re muddling through, which is a lot better than many dared hope a year ago.

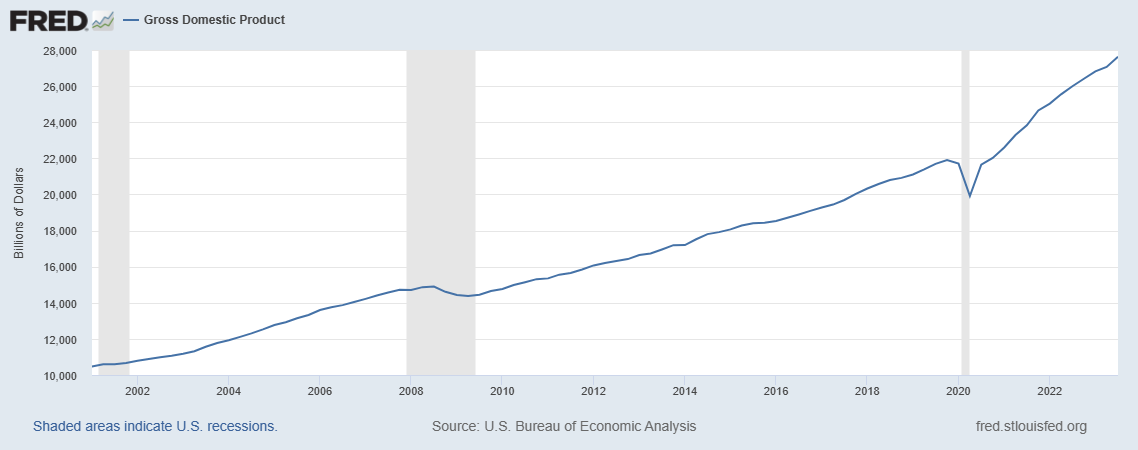

But that’s just the stock market. Unemployment is at historic lows below 4%. GDP is on a tear:

I understand that many prices have risen in recent years and not come down, high mortgage rates are making things tough for first-time homebuyers, and our 401ks aren’t growing as fast as they were. But we also just deflated a massive bubble in the tech sector, survived a global pandemic, partially tamed inflation, and yet the economy as measured by GDP is stronger than ever, and virtually everyone who wants a job has one. All things considered, that seems like rather good news, and one could say Biden has managed the hand he was dealt rather well.

Remember, the economy lags policy. The forces powering the economy in the first couple years of a presidential term likely have far more to do with existing trends and previous administrations’ policies than anything passed by the new administration. A Trump-reelection will not bring back the magic unicorn of low inflation and low interest rates. And if the Trump economy was really the Obama economy with a shot of adrenaline followed by a crash, maybe let’s not assume a do-over is a good idea.